Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

In our relentless effort to identify mispriced stocks with upside potential on behalf of our clients, Causeway has expanded fundamental coverage to include the vast and diverse domestic Chinese market. From an equity research perspective, China domestic A share companies represent a challenge to cover in depth, but we believe they present an enormous opportunity. After nearly 300 fundamental research meetings with Chinese companies since early 2018, we have identified an expanding list of well-run Chinese companies. Our key takeaways from our most recent China company meetings are summarized in this China Research Journal.

Returnees: Seizing a Golden Opportunity

On a recent two-week research trip to China, as escalating US-China trade tariffs threatened global growth, we interviewed senior management of 42 Chinese companies in the healthcare, technology, industrials and consumer sectors. We heard firsthand about the economic pain from the trade war, and the resulting redoubling of efforts by many Chinese companies to achieve independence from American suppliers. We met with founders of recently-listed and other ambitious Chinese companies. Many managements told us that the trade war brings a “golden opportunity,” giving them a chance to scale their businesses as Chinese customers substitute them for American suppliers.

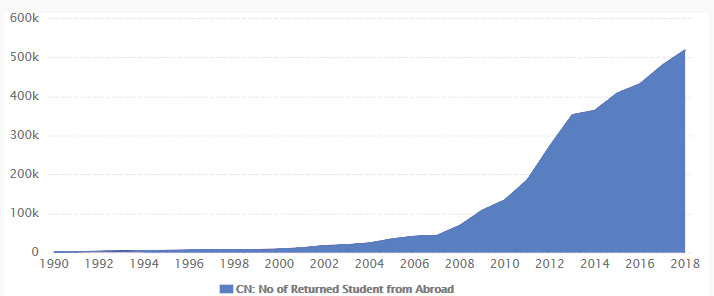

Perhaps most striking were our interactions with members of the expanding “returnee” population. Typically graduate-level educated, and US-trained, these entrepreneurs have returned to China to capture not just abundant funding (and seemingly indiscriminate valuations), but also a well-educated, hard working and productive labor force. An increasing percentage of foreign-educated and trained talent is returning to China due in part to the favorable domestic environment for Chinese growth companies, aided by generous public and private sector support. In 2018, over half a million students returned to China from abroad, a more than 40% increase from five years prior.

Key insights

- The US-China trade war has resulted in the redoubling of efforts by many Chinese companies to achieve independence from American suppliers and scale their businesses.

- An increasing percentage of foreign-educated and trained talent is returning to China due in part to the favorable domestic environment for Chinese growth companies.

- With global institutional investors expanding research coverage of A share companies, we believe valuations will ultimately converge to levels consistent with global industry averages. We are convinced that returns to active management appear promising in this vast market.

Homeward Bound: Foreign-Educated Chinese are Returning to China in Growing Numbers

Source: CEICDATA.COM | Ministry of Education

Those companies that facilitate China’s state industrial policy to catch up with—then surpass—Western technological prowess in advanced industries attract the most investment and subsidies. From our research, we believe that US-imposed trade friction and immigration constraints likely have amplified the returning talent trend. Returnees often bring “know how” and academic and business connections and can attract funding globally. We expect the returnees will continue to have influential roles in the prosperity of many private sector Chinese A share companies.

Nanjing: Technological Ambition in an Ancient City

On day one of our trip, we arrived in Nanjing, Jiangsu Province, a city of approximately seven million people on China’s eastern seaboard. The more enterprising Chinese cities have created public-private partnerships, and Nanjing wants to be part of the action. The city’s local officials are responding to national goals in innovation and technological expertise. The most ambitious startup companies can access Nanjing’s array of benefits: development zones (with simplified company registration and lower regulation), incubators, venture capital funding, research subsidies (rebates on research and development (R&D) expenses), public-sector purchases of products and services, creation of local technology training centers, access for employees’ children to the best local schools and apartments for employees, among numerous other benefits. Cities across China are competing against each other with money and other resources to attract top talent and transform themselves into innovation centers. In response, well-trained, experienced professionals across an array of industries—especially in technology—are returning to China to take advantage of the flood of public and private sector support. They want an ambitious and hardworking labor force and the accelerated opening of domestic Chinese capital markets to foreign investment. Specific to China, some venture capital funds sponsored by city and/or provincial governments seek economic growth and local employment, and not an explicit financial return.

NKF: A Leading Drug Manufacturer Meeting Rising Global Demand

On our visit to the Nanjing High Technology Zone, Causeway research met returnee Tang (Eric) Yong Qun, CEO and chairman of Nanjing King Friend Biochemical Pharmaceutical Company (NKF). With a master’s degree from Stevens Institute of Technology in New Jersey, Eric Tang and his mother, Juhua Xie, control the company with – according to Bloomberg- a combined 48.5% stake. Given the company’s over US$4 billion market cap, this ownership stake makes the CEO and his family first generation billionaires overseeing a business with over 700 employees. Jiangsu Province, via its development fund, owns 20% of NKF, with the rest of the company’s equity widely held. NKF researches, develops, produces and sells active pharmaceutical ingredients (API) and sterile injectable products. Established in 1986 as one of the world’s leading manufacturers of heparin-related APIs, NKF has grown into a fully integrated API and injectables manufacturer in multiple therapeutic areas including critical care and oncology. Used as an anti-coagulant, heparin is a biological product derived from pig intestines. NKF currently controls approximately 20% of the world’s heparin supply. According to management, global demand for the drug has grown 3% per annum in volumes over the past five years.

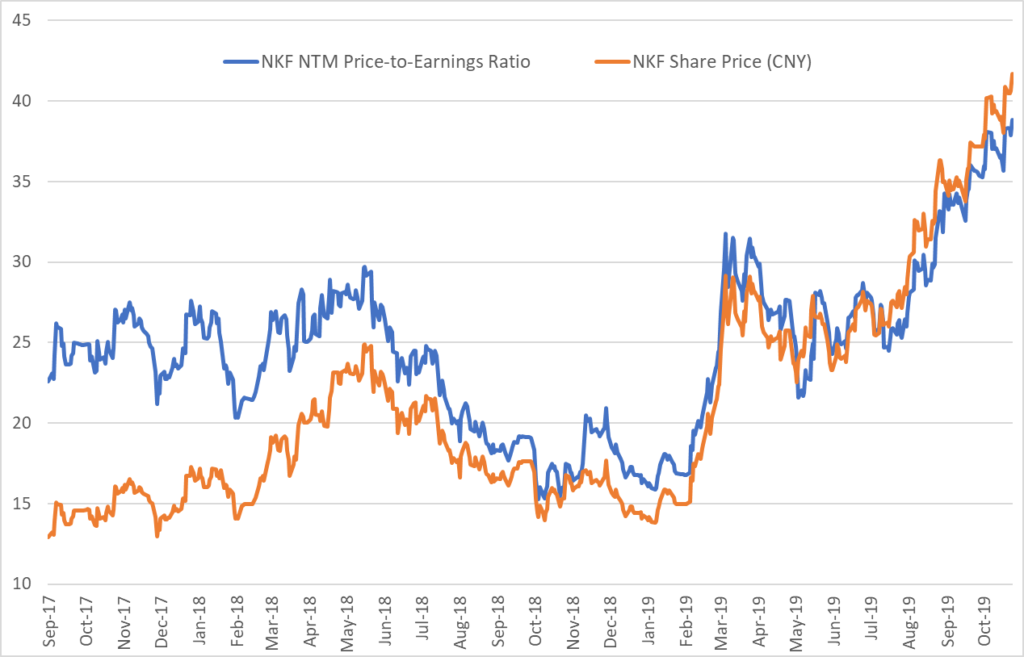

The Soaring Valuation of NKF

Source: FactSet

The growth rate is even faster in emerging countries, especially among China’s roughly one billion insured population where use of heparin should likely grow another 50% before it slows to developed country growth rates. There are no substitutes for heparin in dialysis and in many types of surgeries. With the US as its largest market, NKF’s entire heparin supply chain must be certified by the US FDA. The US hasn’t added pharmaceutical products to the tariff list and won’t – we believe- to avoid self-imposing a heparin shortage. Listed solely on the Chinese A share market, NKF trades at an exceedingly high valuation on a next-twelve-month price-to-earnings ratio of 39x, having returned 190% in local currency terms year-to-date through October 31st. A global savings glut, as well as trapped savings in the Chinese market, imply that NKF can get access to plenty of capital for expansion.

Maxscend Microelectronics: A Rising Beneficiary of Accelerated Chinese Self-Reliance

Headquartered in Wuxi Research & Development Center in a Jiangsu High Tech park, seven-year-old Maxscend Microelectronics (Maxscend) produces and sells smart phone radio frequency (RF) switches, low noise amplifiers, RF front end chips and electronic products. Former chief technology officer, now chief operating officer, Feng Chenhui, met with us to explain his company. The three founders, including Mr. Feng, plus company employees, own over 36% of the company according to Bloomberg. Mr. Feng has over $400 million of newly-minted wealth following the company’s IPO in June 2019 on the Shenzhen Stock Exchange. He explained to us that the US-China trade war has been a boon to RF chip manufacturers. Their Chinese customers, currently blocked from their US suppliers, now will take a chance on Maxscend as a chip designer. Feng and his Silicon Valley-trained returnee co-founders have seen China transform from a country devoid of chip design experience 15 years ago to one that currently employs many people with the necessary design skills. In a very short R&D cycle, the company must react quickly to customer demands, and its engineers work more than 12-hour days, six days a week. Like so many companies we have met, Maxscend overcomes areas where they lack technological expertise through trial and error, in what they call a “brutal competitive industry” where it’s “easy to make a mistake.” Although Maxscend has set up an office in the US, Mr. Feng expressed concern that if the US and China do not work together, each country will need to build duplicate systems, thereby wasting resources, time, etc. The more the US threatens China, said Mr. Feng, the more that Chinese engineers working abroad will choose to return to China. Mr. Feng expects that once supply chains reset, many Chinese companies will lose trust in US suppliers and will not rebuild those supply chains. China wants to be self-reliant in semiconductors, and the trade war and supply chain disruption is accelerating that effort. Although Mr. Feng admitted that the company’s share price is richly valued, he added that this high valuation attracts the attention of potential young recruits.

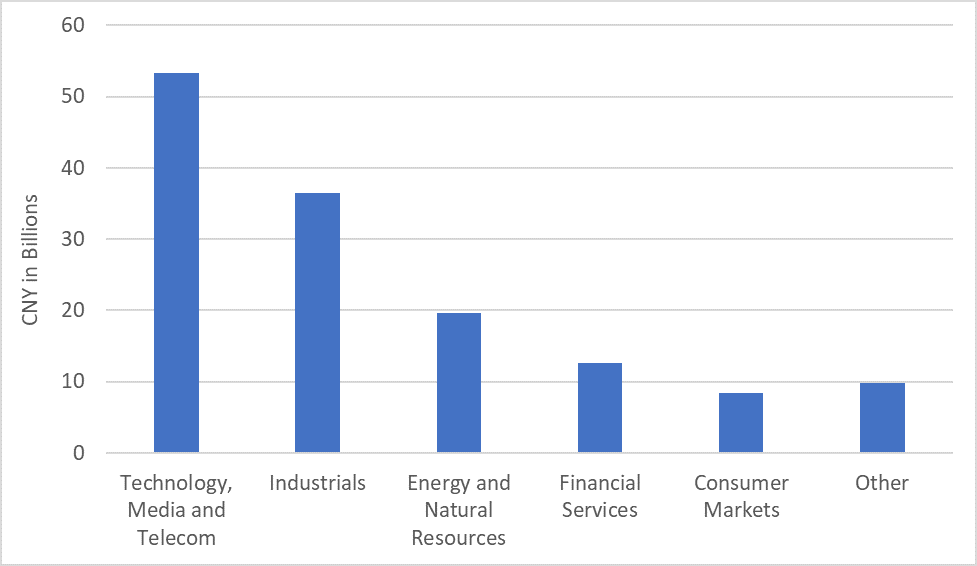

China A IPOs in 2019 by Sector

Source: KPMG. Data as of September 13, 2019

Shanghai: A First-Tier Hub

We finished week one in the sprawling Shanghai municipal region, where 26 million people live in the urban areas, and millions more in the surrounding towns. As China’s commercial capital and financial center, returnees flock to Shanghai, many joining the technology sector.

Advanced Micro-Fabrication Equipment Inc.: The Homegrown Advantage

Founded in 2004 in a Shanghai suburb, Advanced Micro-Fabrication Equipment Inc. (AMEC) supplies its equipment to global semiconductor manufacturers and leading companies in adjacent high-tech sectors like solid state lighting. The company specializes in equipment used to develop and produce micro-sized and nanoscale-sized “very large-scale integration,” defined as the process of creating an integrated circuit (IC) by combining thousands of transistors on a single chip. AMEC focuses on vapor deposition and plasma etching products. Initially funded by Qualcomm Ventures and other investors, AMEC was one of the first companies to list on the Shanghai Stock Exchange Science and Technology Innovation Board (STAR Market). AMEC is one of the few core equipment suppliers that engages in high-end IC processing in China. Causeway research met with AMEC’s CFO, Chen (Andrew) Weiwen, a partly-US educated, and US-trained, returnee to China. He and his colleagues recognize the market opportunity in China to supply local semiconductor fabrication plants. Chinese capital is looking for domestic equipment suppliers. Self-sufficiency will be a byproduct of achieving scale in the massive Chinese market, then AMEC plans to expand abroad. Trade tensions have made AMEC’s customers want more Chinese suppliers and lower their dependency on US technology and US equipment. This US$5 billion market cap company trades at a 2021 price to earnings ratio of over 100x.

Implications for Global Investors

We have described only three notable meetings from our trip, but we have numerous files with information about fascinating businesses, many of which are new to global investors. The Chinese market is huge. China A (combined Shenzhen and Shanghai stock exchanges) is the second largest equity market globally measured by market cap and cash trading volumes, just ahead of Japan. Add Hong Kong-listed Chinese H shares and Chinese securities listed on US and other non-China stock exchanges, and no other non-US market can rival its size. New to China A shares, foreign investors in aggregate own less than 4% of the market. The CSI300, an index of the 300 largest most liquid China A share stocks, has returned an average of 8.3% per annum for the past five years through October 31, 2019, versus 8.2% for the MSCI World Index and 10.8% for the S&P 500 Index (SPX). Recently, returns have improved as the CSI300 has risen 29% versus 23% for SPX in the year-to-date period through October 31, 2019. The MSCI inclusion factor (the extent to which China A stocks are in the MSCI Emerging Markets Index) keeps rising; the most recent hike was from 10% to 15% in August 2019. When China A stocks are 100% included, we project that China will be over 45% of the MSCI Emerging Markets Index, versus 32% today.

Causeway China Research has expanded to address this challenge with dedicated China investment professionals collaborating with each of our six fundamental research cluster groups. We aim to identify companies of interest, both as candidates for existing global, international and/or emerging markets portfolios (where permitted) as well as sources of competitive information to improve our understanding of non-Chinese portfolio companies.

After nearly 300 research meetings with Chinese managements since early 2018, we have identified an expanding list of well-run companies (some with reasonable valuations) and corporate governance meeting our standards. This list of China A share company buy candidates will grow as we increase our efforts to scour the country for the misunderstood – and the underpriced. The companies we featured in this paper are not in client portfolios due to their high valuations. With global institutional investors expanding research coverage of A share companies, we believe valuations will ultimately converge to levels consistent with global industry averages. We are convinced that returns to active management appear promising in this vast market.

This market commentary expresses Causeway’s views as of October 29, 2019 and should not be relied on as research or investment advice regarding any stock. These views and any portfolio holdings and characteristics are subject to change. There is no guarantee that any forecasts made will come to pass. Forecasts are subject to numerous assumptions, risks and uncertainties, which change over time, and Causeway undertakes no duty to update any such forecasts. Information and data presented has been developed internally and/or obtained from sources believed to be reliable; however, Causeway does not guarantee the accuracy, adequacy or completeness of such information.

The S&P 500 Index is a stock market index that measures the performance of 500 large companies listed in the United States. The CSI 300 is a capitalization-weighted stock market index designed to replicate the performance of top 300 stocks traded in the Shanghai and Shenzhen stock exchanges. The MSCI World Index is a free float-adjusted market capitalization index, designed to capture large and mid cap segments across 23 developed markets countries, including the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index, designed to measure the performance of the large and mid cap segments of 26 emerging markets countries. The indices are gross of withholding taxes, assume reinvestment of dividends and capital gains, and assume no management, custody, transaction or other expenses. It is not possible to invest directly in an Index.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.