Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

Uncertainty surrounding Brexit has contributed to compelling valuations for UK stocks. At Causeway, we build portfolios on a bottom-up basis through rigorous fundamental research and quantitative analysis. Although our strategy is designed to identify company-specific investment opportunities, we acknowledge that political events such as Brexit can impact our portfolios, particularly in the short term. In this update, we review the Brexit timeline and assess the potential impact of Brexit on Causeway’s global and international value portfolios.

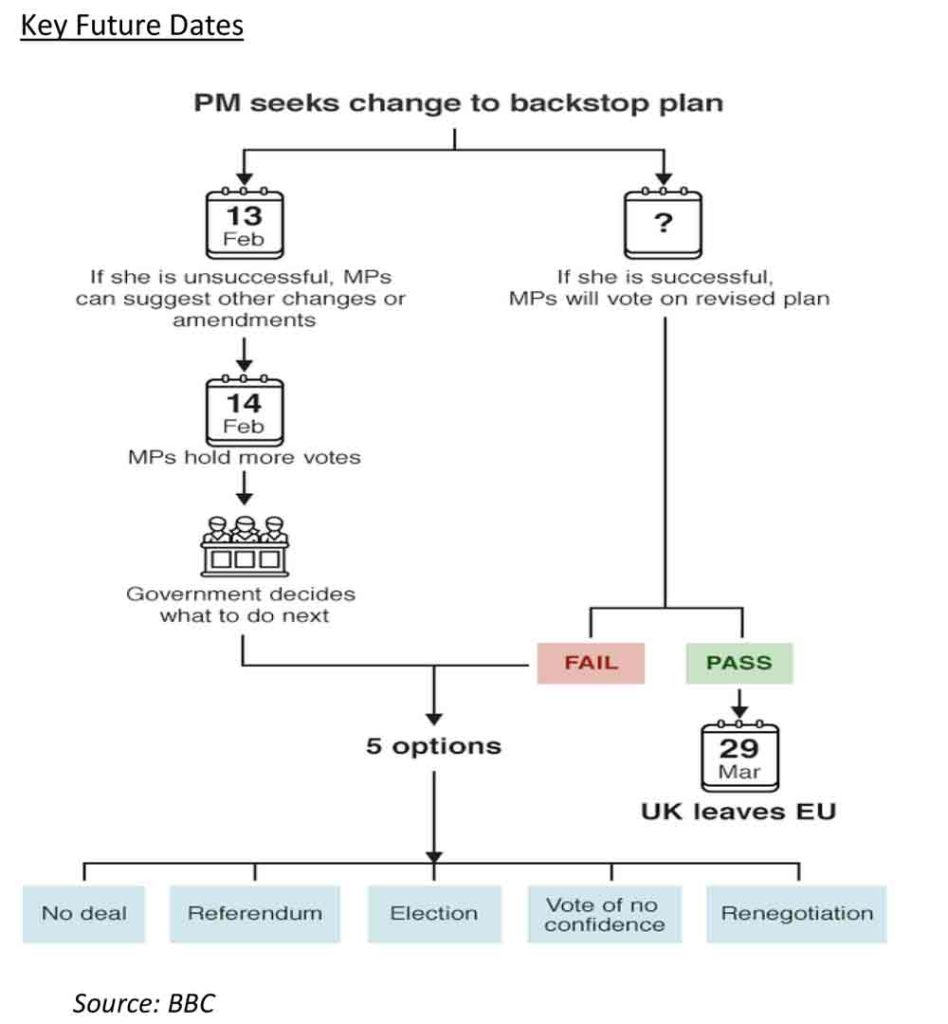

Brexit summary and key dates going forward

On June 23, 2016, Britons voted to exit the European Union (“EU”) by a vote of 52% to 48%. Article 50 of the EU treaty, which outlines the procedure for an EU member state leaving the union, was triggered in March 2017. The EU and the UK have until March 29, 2019 to agree on the terms of the separation. The UK Parliament must pass Prime Minister Theresa May’s Brexit deal. Ms. May presented a proposed deal to Parliament on January 15, 2019 and Parliament voted to reject the deal. Ms. May is expected to present a revised proposal to the House of Commons on February 13, 2019. With the exit date deadline approaching, Parliament has three primary options: 1) vote in favor of the revised deal (we believe this is most likely), 2) reject the revised deal and use a variety of alternatives to postpone the exit, or 3) exit with no deal. Given the negative consequences of a hard Brexit, we expect the UK to approve the deal or postpone a decision, but we do not expect a disorderly Brexit.

Potential Brexit scenarios and estimated market response

The UK electorate’s June 23, 2016 decision to withdraw from the EU surprised most investors, including Causeway. The pound sterling decline impacted UK stocks broadly in the days following the vote. However, the stock returns were more differentiated over longer periods. UK-based businesses that generate substantial portions of their revenues outside the UK generally performed better than those with more locally generated revenues. Looking forward, we assess the different scenarios below.

We currently believe a soft Brexit is the most likely outcome.

Hard Brexit – the UK exits the EU without a deal in place on March 29, 2019

In the short term, a disorderly Brexit would be very disruptive to the UK economy and financial markets. The majority of UK Members of Parliament (MPs) have indicated they are against this outcome. We currently believe this scenario is unlikely, as the short term economic ramifications would threaten the Tory Party’s advantage.

Soft Brexit – scenarios include renegotiation of the Brexit deal and postponement of the Brexit process past March 29

We currently believe a soft Brexit is the most likely outcome. In order to extend the March 29 deadline, the UK would request an extension and all 27 EU countries would need to agree. Mervyn King, former Governor of the Bank of England, described the divisions within the UK government and the challenges in drafting a deal that receives the required support. These factors increase the probability of the UK requesting an extension past the March 29 deadline.

No Brexit – the UK cancels Brexit and remains in the EU

The European Court of Justice has ruled that it would be legal for the UK to unilaterally revoke Article 50, thereby cancelling Brexit. This would likely be proceeded by a second referendum. If the majority of UK citizens elect to remain in the EU, the government would have the public support needed to cancel Brexit and remain in the EU.

From a valuation perspective, we believe UK stocks already discount an uncertain future, including a hard Brexit.

Short Term – less than 1 week

In the short term, we believe that the pound sterling would weaken in a hard Brexit scenario.

Medium Term – up to 24 months

Even with a disorderly Brexit, we believe equity valuations will likely adjust to the new reality over the medium and long term. From a valuation perspective, we believe UK stocks already discount an uncertain future, including a hard Brexit. Over the medium-term, and longer, horizons, stock selection should be an important driver of performance regardless of the Brexit outcome.

As active managers continuously searching for attractive opportunities, our portfolio positioning changes over time. The various Brexit scenarios will present opportunities and risks. Our portfolios will evolve as we seek to take advantage of new opportunities on behalf of our clients.

UK Stocks: Compelling Valuations

UK stocks de-rated severely in 2018, and are currently trading at the cheapest levels in the past 25 years (except during the global financial crisis “GFC” in 2008-9) on a dividend yield basis. Many UK dividend yields are nearly equivalent to price-to-earnings (P/E) multiples. Measured by the earnings yield/bond yield premium, the UK stock market has only been cheaper twice in the past 100 years (during World War I and World War II)*. The decoupling of UK free cash flow yields from other developed markets is evident in the chart below.

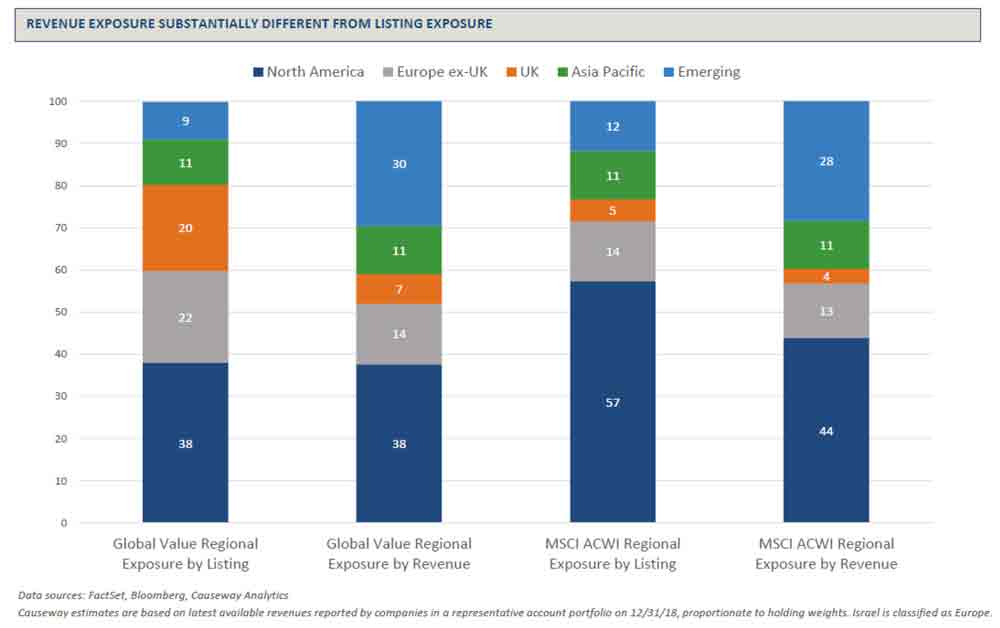

The UK exposures for both the Causeway representative portfolio and the MSCI ACWI Index are lower on a revenue basis than on a listing basis.

Within a Causeway Global Value Equity representative portfolio, the overweight to the UK versus the MSCI ACWI Index is more significant when measured by listing (15% overweight) than when measured by the revenue sources of the portfolio companies (3% overweight). Additionally, the UK exposures for both the Causeway representative portfolio and the MSCI ACWI Index are lower on a revenue basis than on a listing basis. UK-domiciled companies in sectors such as capital goods, energy, materials, pharmaceuticals, and food beverage and tobacco have diverse global operations and often generate most of their revenues outside the UK.

Fundamental Brexit Risk Analysis

Of Causeway’s UK-domiciled holdings in its fundamental strategies – Global Value and International Value – we believe UK financials stocks may be most exposed to Brexit risk. For those holdings, we have evaluated the investment cases under stress tests that estimate the impact of a hard Brexit. Although we do not currently expect a disorderly exit, even in this scenario we have identified upside potential in current share prices.

We continue to monitor the political process, but believe that many UK stock valuations are attractive, especially relative to peers in others markets.

Banks

The Bank of England (“BOE”) performs annual stress tests that we believe are more nuanced than stress tests we could conduct internally, given the application of stress to different books of business. These test the banks’ entire books, not just the UK exposure. The BoE’s financial policy committee deems the Annual Cyclical Scenario “ACS” test performed to be sufficiently severe to encompass the disorderly Brexit scenario. Macroeconomic shocks in the ACS test include: UK gross domestic product falls by 4.7%, the UK unemployment rate rises to 9.5%, and UK real estate prices fall by more than 30%. The scenario also includes a sudden loss of overseas investor appetite for UK assets, a 27% fall in the sterling exchange rate index and the BoE’s Bank Rate rising to 4%. After conducting this stress test, the BOE noted the UK banking system’s resilience. We are comfortable with the capital positions of the UK bank holdings in our fundamental portfolios in this scenario.

Insurers

For the UK-listed insurers in Causeway’s fundamental portfolios, we are interested in the impact of stress on the companies’ ownership of bonds and credit instruments. Our primary focus is on what would happen to tangible book value and solvency ratios in case of a repeat of the bond default environment of 2001/2002 (which was worse than 2008, where most of the losses were on loan exposures) extended over three and five year periods. We believe the estimated declines in tangible book value will not require the insurers to raise capital. Despite the stress, solvency levels for these companies should still meet regulatory standards and are well within management’s target ranges. We believe these are draconian scenarios because even in a hard Brexit, credit default levels would not necessarily increase to the levels experienced in 2002. We continue to monitor the political process, but believe that many UK stock valuations are attractive, especially relative to peers in others markets.

*Citi Research, January 3, 2019, “Global Equity Road Ahead”

This market commentary expresses Causeway’s views as of February 8, 2019 and should not be relied on as research or investment advice regarding any investment. These views are subject to change, and there is no guarantee that any forecasts made will come to pass. Forecasts are subject to numerous assumptions, risks and uncertainties, which change over time, and Causeway undertakes no duty to update any such forecasts. Information and data presented has been developed internally and/or obtained from sources believed to be reliable; however, Causeway does not guarantee the accuracy, adequacy or completeness of such information.