Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

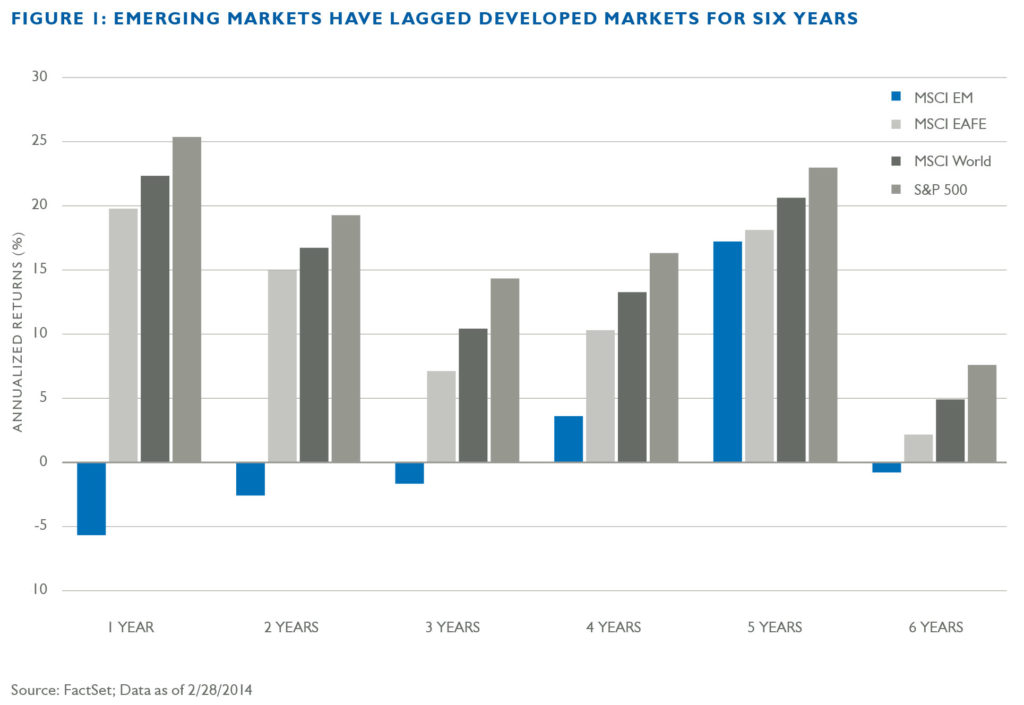

After six cumulative years of lagging returns versus developed market indices, why bother with emerging markets? Read how we continue to find opportunities in the struggling asset class.

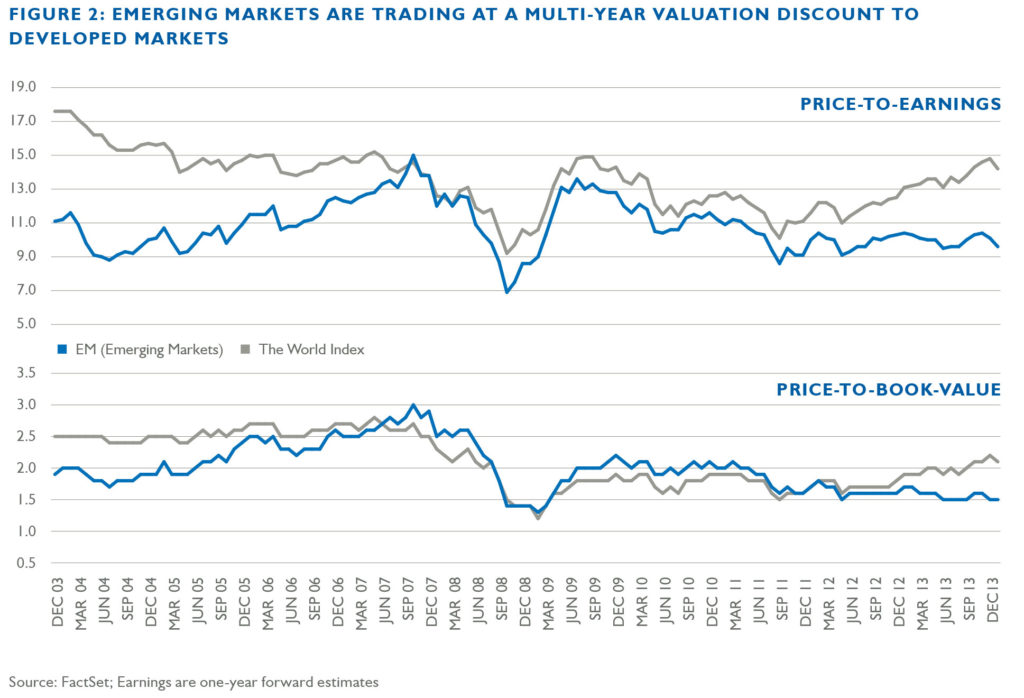

Emerging markets equities have certainly cracked from a valuation perspective and trade at a price-to-earnings ratio over 30% lower than developed markets – the largest valuation gap since mid-2005.

After six cumulative years of lagging returns versus the MSCI World, MSCI EAFE and the S&P 500 Indices, one might ask, why bother with emerging markets? What will break the spell and reverse the post-2007 overall period of underperformance? Emerging markets equities have certainly cracked from a valuation perspective and trade at a price-to-earnings ratio over 30% lower than developed markets – the largest valuation gap since mid-2005. Some of the performance drag reflects a loss of investor confidence, as several emerging markets are burdened by economic and/or political setbacks. However, the current economic travails of many emerging markets are not unusual. These countries have spawned domestic private and public sector credit excesses in prior cycles, leading to substantial – albeit temporary – market volatility. Political tensions, such as the recent conflict in the Ukraine, are typically buying opportunities, not reasons to abandon the asset class.

Despite the recent outflow of funds from emerging markets, Causeway currently favors an increasingly larger allocation to the asset class in its global opportunities strategy. We use the MSCI All Country World Index, with its 10% emerging markets weight as a starting point. In a global context, Causeway’s allocation model favors emerging markets as a result of attractive relative valuation and earnings growth characteristics versus developed markets, improving macroeconomic factors and the rising level of global risk aversion (measured by the CBOE Volatility Index (VIX) and the emerging market bond index yield spread over US Treasury bonds). Admittedly, we are adding emerging markets exposure very gradually to client portfolios in our global and international opportunities strategies. Due to the importance of the “top-down” asset allocation decision, we must answer the following questions: How much of the decline in relative real gross domestic product (GDP) growth rates (emerging versus developed markets) is cyclical versus structural? To what degree can we rely on historical valuations of these markets– especially if structural changes are occurring?

Emerging markets achieved their best performance on record from 2002-2007 when the MSCI Emerging Markets Index rose by a cumulative 361%. The developing regions boasted improving external and fiscal balances, as well as rapid growth in sales and earnings.

Since then, imbalances have widened again for several emerging countries due to rapid credit-fueled domestic demand growth and weak domestic demand in the United States, Europe and Japan. As the overall trade surplus in the developing countries has fallen, much of the emerging bloc has receded into current account deficit (importing more than they export), with a few countries suffering from serious external imbalances (Turkey, South Africa, Brazil, and India, for example). To add insult to injury, foreign investors aren’t waiting to see how it all pans out. When investors get nervous, they run for the exits. Emerging markets are paying the price for exchange traded fund (ETF) liquidity—suffering volatility inflamed by the ability of investors to sell ETFs quickly. Of the 22% drop in the net assets of the iShares MSCI Emerging Markets ETF in 2014 to date, only 6.5% is due to the total return of the fund. Outflows explain the bulk of the shrinkage in net asset value. We estimate that two prominent emerging markets ETFs lost $25 billion—more than 20% of their net assets—to outflows in 2013 and this year to date, combined.

To explore the cyclical versus structural question in emerging markets, we spoke to Causeway portfolio managers Arjun Jayaraman, Duff Kuhnert, and Joe Gubler.

Remember that stock markets discount future events well in advance. Markets will reflect any economic recovery in the emerging countries several quarters before we see the improvement in the data.

Arjun, at what point will emerging markets become cheap enough to warrant a more aggressive allocation than you currently advocate for Causeway’s international and global opportunities clients?

AJ: The valuation discount, plus the earnings momentum and increasing global risk aversion factors, have tipped our asset allocation model to favor an overweight in emerging markets. As with any economic down cycle, adjustments invariably occur. To cure for credit excesses, central banks in the inflation-plagued countries have started a phase of monetary and credit contraction—and that dampens economic activity. The tight credit conditions should ultimately force companies to boost productivity and enhance returns on capital to re-attract foreign investment. With inherent growth advantages versus the developed world, the emerging countries are magnets for foreign capital. In a few years, asset prices should increase again as credit expands. That’s the cycle. Remember that stock markets discount future events well in advance. Markets will reflect any economic recovery in the emerging countries several quarters before we see the improvement in the data.

But what has changed about the emerging markets since 2007 that explains their disappointing cumulative returns?

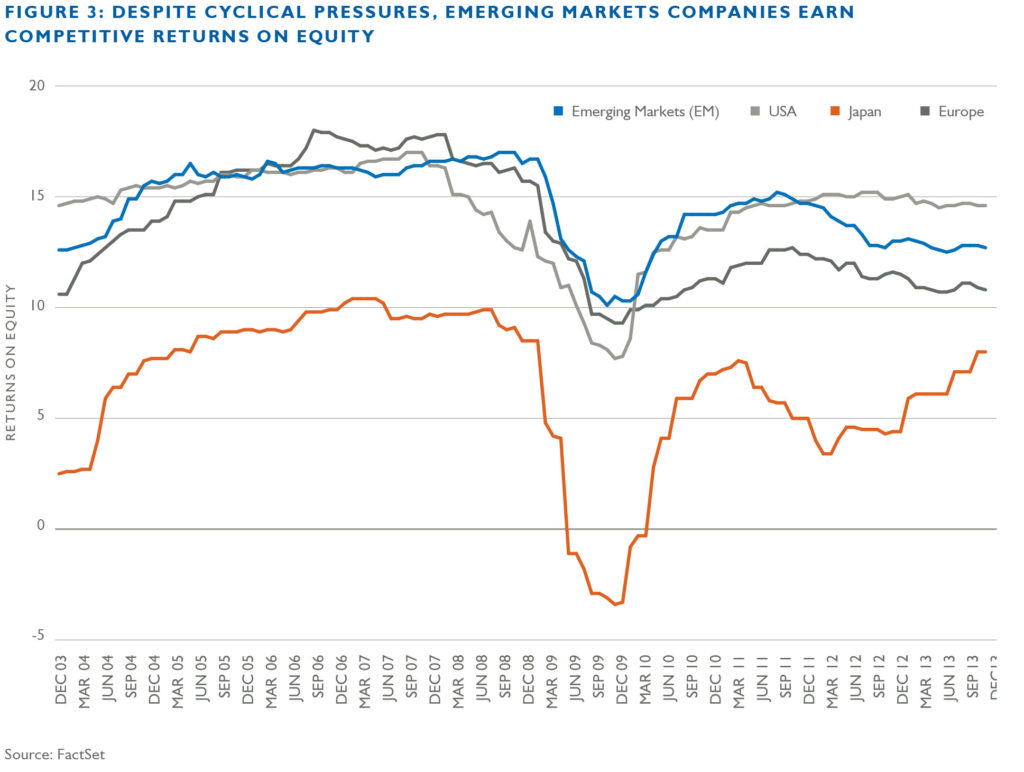

DK: Some critics claim that many emerging markets currently suffer from low and declining returns on capital, a byproduct of unsustainably fast growth. Inefficient investment typically leads to sinking returns on investment, triggering capital flight (from a low-return region) to one offering better returns. We do not expect this situation to persist. Although returns on equity (ROEs) in emerging markets have not recovered to pre-2008 levels, they are still above longer-term averages, and are superior to ROEs in Europe and Japan. Narrowing profit margins have played the key role in the depressed emerging market ROEs in the past few years, as tight labor market conditions prompted wage increases. We believe this trend is cyclical, not structural. Some of the larger emerging markets countries, such as Brazil and China, avoided the worst of the 2008 financial crisis and subsequently boomed, creating upward wage pressure. In the meantime, the slow recovery in the developed world led to large productivity gains and weak wage gains (causing developed market margins to expand). For those companies competing on a global scale, the natural selection of markets will favor those firms achieving increases in productivity, allowing them access to low-cost capital. Over the next few years, we expect the profit margin difference between emerging and developed markets companies to narrow. Regardless, emerging markets companies retain a clear advantage versus developed peers in terms of revenue growth. Overall, financial leverage is also significantly lower in emerging markets relative to the developed world. As capital markets continue to develop and strengthen in emerging economies, leverage should increase, providing further support to ROEs of companies in emerging markets.

AJ: As economies mature, low return investments naturally attract less capital than those with high returns. This is a normal path of development, and we believe not a structural flaw with emerging markets.

JG: Many emerging country currencies have devalued versus the US dollar over the past three years. This should help reverse the negative current accounts and improve the competitiveness of these countries. Indonesia, for example, has seen a fall of 17% in the rupiah versus the dollar over the past year, coinciding with a narrowing of the country’s trade deficit. Brazil’s trade account is roughly in balance, although its current account is slightly negative. In contrast, South Africa and Turkey each have a steeper road ahead economically. However, they also have some of the most favorable demographics.

You haven’t yet mentioned China. Are its problems also cyclical – and temporary?

AJ: The changes in the Chinese economy, including the shift from export-driven to consumer led- are structural, and will take many years. The country still has a positive current account balance. I admit that the rising levels of public and private sector debt are concerning. The question we ask ourselves is whether China has a probability of experiencing a collapse of its financial system. China’s rapidly expanding shadow banking sector includes trust (savings) products, which will likely experience debt defaults. But problems in the shadow banking sector don’t appear large enough to topple the country’s planned economy and disrupt its (closed) capital account.

JG: According to data from BCA Research, the total size of assets managed by various Chinese financial institutions has risen from RMB8 trillion in 2008 (less than 40% of household bank deposits) to RMB36 trillion in 2013 (77% of household savings deposits). To put that in perspective, at about 30% of the formal banking sector, the Chinese shadow banking system is far smaller than in most other major economies.

DK: We are watching this situation carefully. China has enjoyed tremendous growth in household wealth. The Chinese have invested their savings in all sorts of domestic projects in real estate and infrastructure, as well as directly in domestic companies. When investments sour, especially the local government infrastructure projects, we expect the central government to backstop the credits. Our confidence in the valuations of Chinese stocks is closely linked to the fiscal strength of the nation.

Important Disclosures

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

The market commentary expresses the portfolio managers’ views as of 2/28/2014 and should not be relied on as research or investment advice regarding any stock. These views and portfolio holdings and characteristics are subject to change. There is no guarantee that any forecasts made will come to pass. Any portfolio securities identified and described do not represent all of the securities purchased, sold, or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.