Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

Prolonged periods of underperformance versus the mighty US equity market have cast a shadow over international equity allocations. With international equities and currencies delivering inferior recent performance and market correlations at high levels, why bother with international markets? In our January 2015 newsletter, we urge our clients to free themselves from regional constraints and invest globally. By definition, an expanded opportunity set of investments brings more buy candidates—and a greater opportunity to capture upside potential. To further our case, our fundamental portfolio managers share some of the global equity opportunities they have identified for 2015.

Invest globally, we urge clients. By definition, an expanded opportunity set of investments brings more buy candidates - and a greater opportunity to capture upside potential.

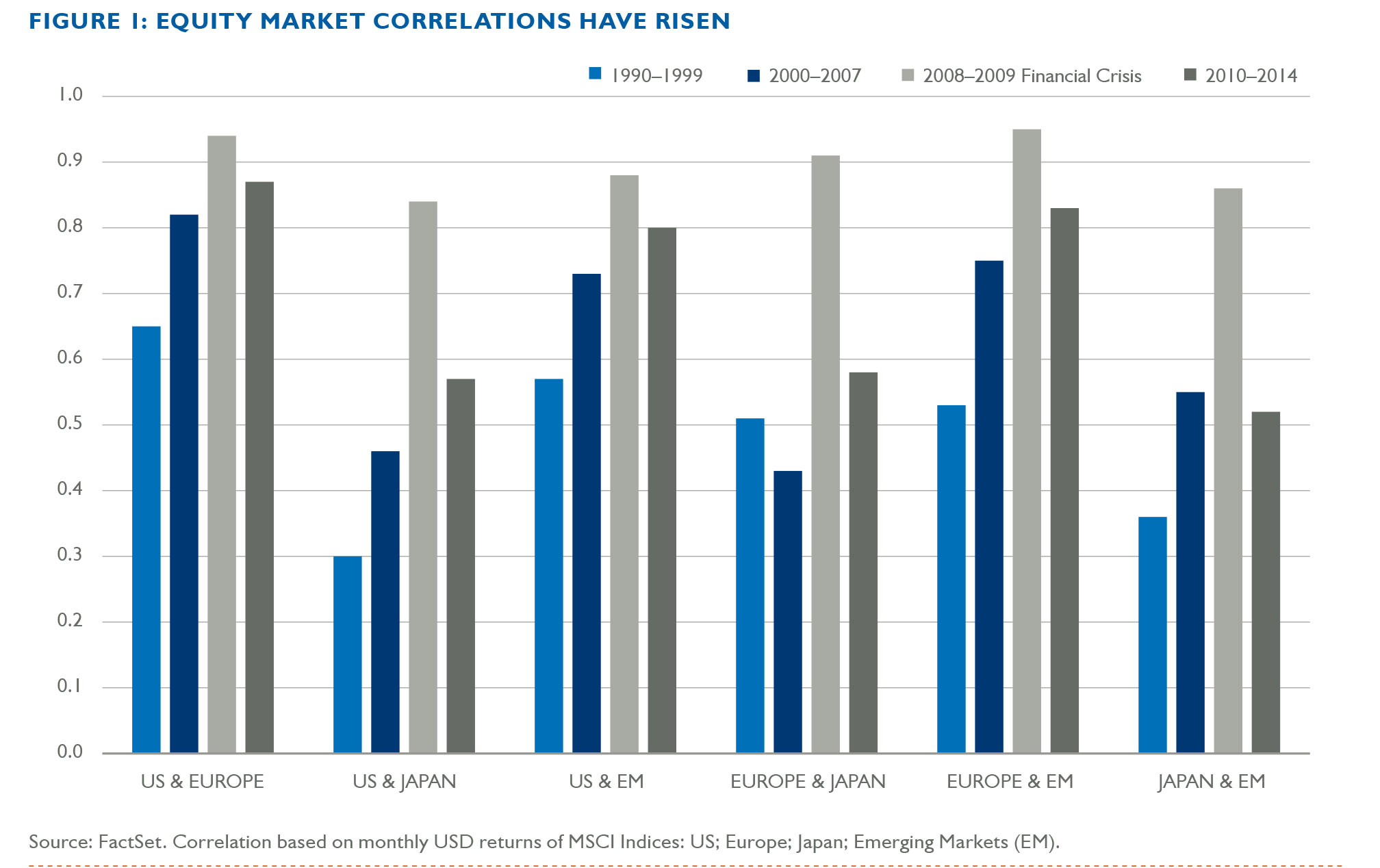

Prolonged periods of underperformance versus the mighty US equity market have cast a shadow over international equity allocations. In these periods of US-market dominance, US-domiciled clients habitually ask us to defend their exposure to foreign markets. With international equities and currencies delivering inferior recent performance, and market correlations at high levels, why bother venturing from home? One could argue that overall superior country and company management continues to distinguish US companies from non-US peers. Furthermore, the recovery in US gross domestic product (GDP) from the 2008 crisis is far more advanced than in any other developed country. These conditions have led to the most de-synchronized global monetary policy in 25 years, according to the global equity strategy team at Credit Suisse*. Perhaps this will allow US stocks to dislocate even further from the rest of the world. Under that scenario, international (both developed and emerging markets) allocations would continue to detract from overall performance.

Over the past decade, our response to “Why invest internationally?” has remained consistent. Invest globally, we urge clients. By definition, an expanded opportunity set of investments brings more buy candidates – and a greater opportunity to capture upside potential, we argue. Over time, we have become convinced that top-down geographic allocations do not benefit clients. Most importantly, these allocations do not incorporate a full array of risk factors; they simply classify stocks in the portfolio by domicile, country of listing or similar criteria. We prefer to invest across as broad a geographic mandate as our clients will allow. We believe that the investment manager may be in the best position to spread geographic (and other) risks in order to obtain the highest projected risk-adjusted return. Despite the dominance of the US equity market this decade, many (and we emphasize many) attractive stocks—especially those likely on the cusp of a cyclical recovery—have proliferated in non-US markets. However, in order to build an optimal portfolio from a return versus risk perspective, buying well-managed companies in various industries globally makes the most sense to us. This portfolio construction process results in a deliberate allocation of risk across multiple factors.

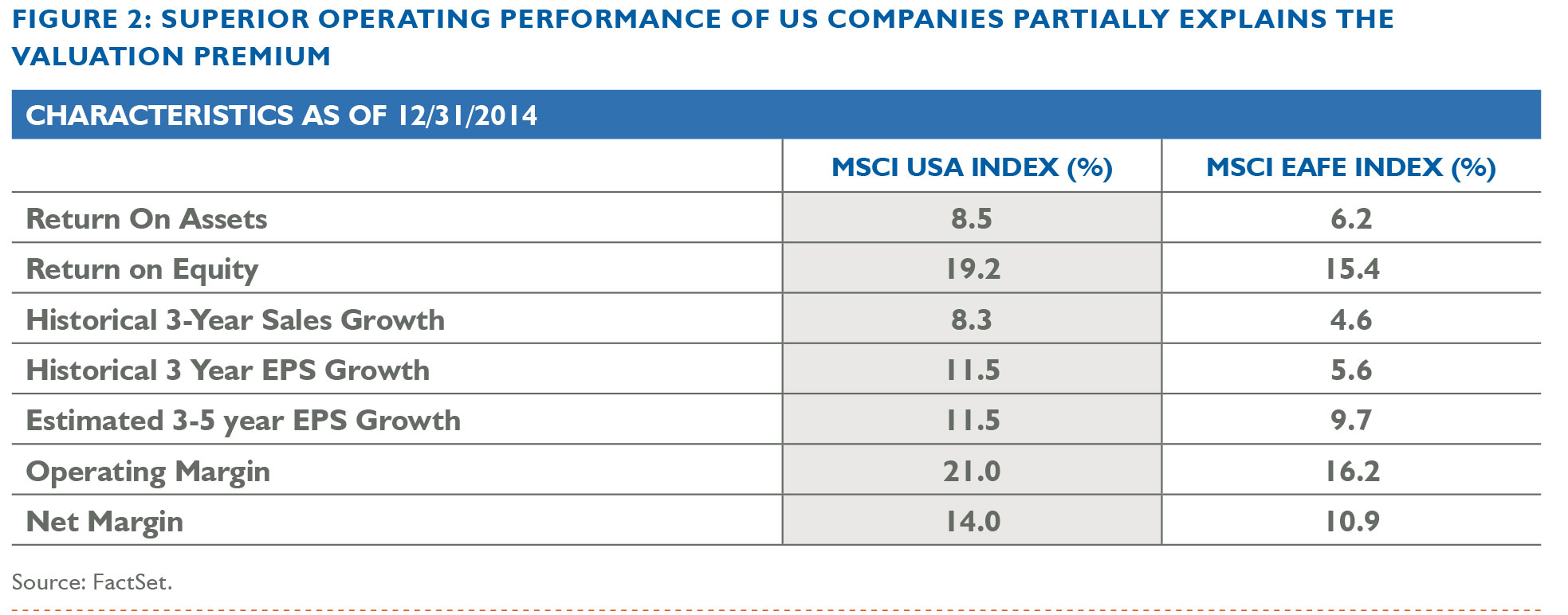

For the past several years, non-US equity markets—both developed and emerging—have traded “cheaper” than the US market. However, that undervaluation has not led to a surge in international equity performance to close the valuation gap. Some of this US valuation premium can be attributed to the average US market constituent boasting superior profit margins, earnings per share (EPS) growth and returns on capital in excess of the non-US developed markets average. The growth gap favoring emerging markets stocks has also narrowed in the recent past.

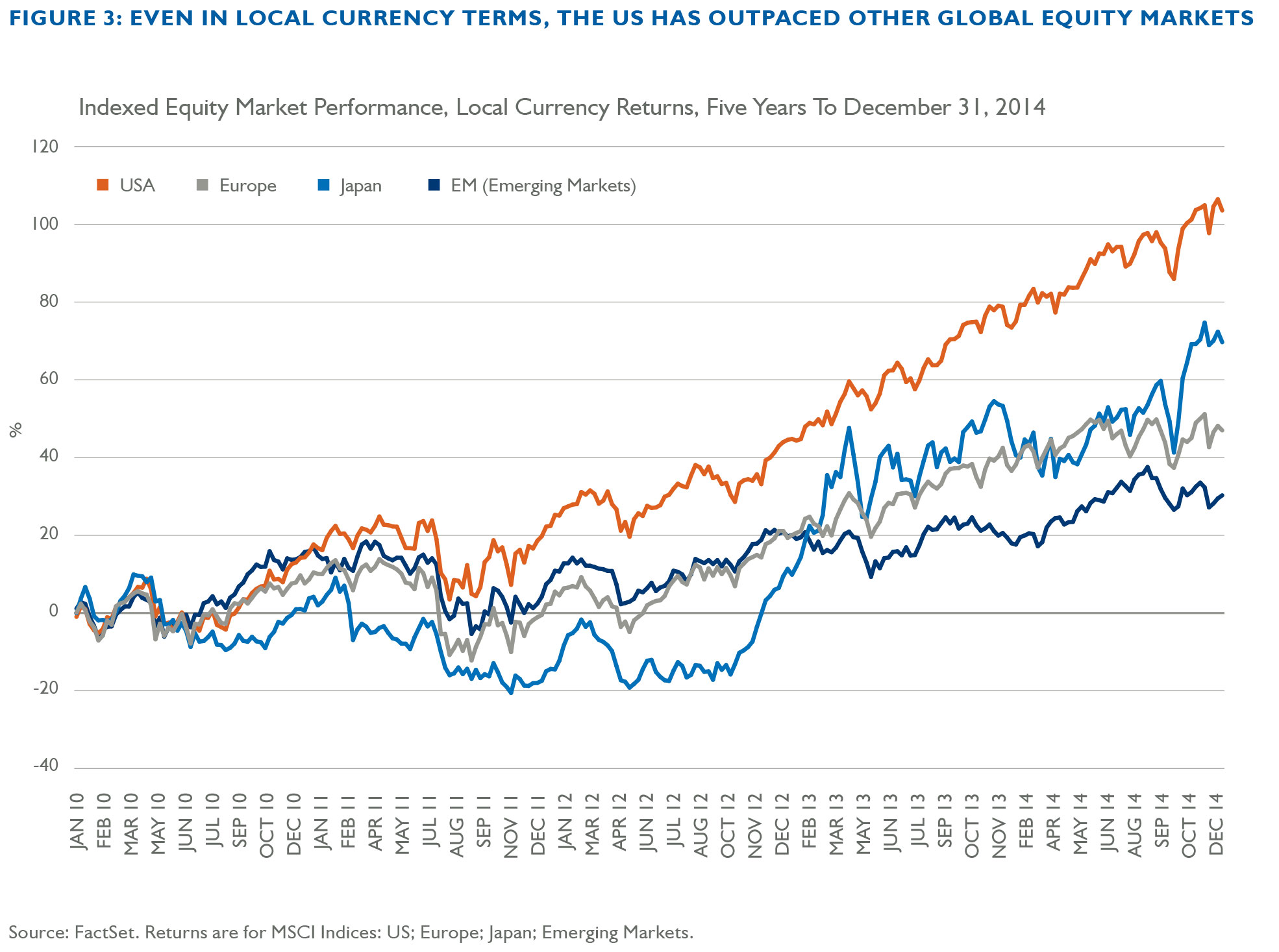

US equity market performance has far surpassed other regions over the past five years, even after adjusting for the rising US dollar.

How much of this recent outperformance by the US market should continue in the next few years? No one knows. But we should ask, if unconstrained by geography, where are the best investment opportunities today? Causeway’s (preferred) mandate, namely “Global Opportunities”, is benchmarked to the MSCI All Country World Index, and increased its exposure in 2014 to emerging markets to over 11% of the total portfolio. US stocks represent approximately 58% of the MSCI World Index, and 52% of the MSCI ACWI Index. By contrast, at December 31, 2014, the Causeway Global Opportunities portfolio had only a 38% exposure to US-listed stocks.

We spoke to Causeway portfolio managers Kevin Durkin, Conor Muldoon, Alessandro Valentini, and Ellen Lee to illustrate the bottom-up portfolio allocation, and explain why we believe that many non-US stocks should have a performance advantage over their US peers in 2015.

A prolonged period of low-cost financing has a habit of fueling asset price inflation, which should support stock prices in regions of monetary expansion (Europe, Japan, and some emerging markets).

Conor, why underweight the US market and US dollar in global mandates? Why take this type of benchmark risk?

CM: We have added disproportionately more non-US stocks into our global portfolios than are represented in a global index, based on our weekly screens, intensive research, and developed markets versus emerging markets analytics. Any hint of a European and/or Japanese cyclical recovery—even if very modest—should inspire buying of a wide array of economically exposed stocks, especially in the financials and industrials sectors. After the information technology and healthcare sectors, much of what fueled US market performance in 2014 had some sensitivity to declining interest rates. US real estate, utilities, etc. are unlikely to have another re-rating upward if—as we expect—the US Federal Reserve tightens monetary policy this year. In contrast, the European Central Bank (ECB) has announced a plan to return to 2012 levels and expand its balance sheet to approximately €3.1 trillion. To reach that target, the ECB will likely need to engage in significant quantitative easing (QE). QE would keep asset yields low (squeezing bank profits), but also would lower the cost of risk. Rising liquidity should work its way into equities. A prolonged period of low-cost financing has a habit of fueling asset price inflation, which should support stock prices in regions of monetary expansion (Europe, Japan, and some emerging markets).

Alessandro, what do you expect to perform well in 2015?

AV: We are searching for (as yet) unrecognized income stocks. For European banks, the last few years of prolonged restructuring, capital rebuilding and huge fines crippled dividend payout ability. With that tough period behind us and our expectations for very modest loan growth, we expect many European banks to increase dividends. Those banks with thriving retail banking and asset/wealth management franchises appear particularly well positioned to restart dividends or slowly increase their payout ratios.

We may also see another satisfactory year in our non-US pharmaceutical holdings. Several of the companies in the portfolio have focused on restructuring or disposing of low-return business segments. In some instances, a rising US dollar might also provide a boost to earnings. Market values in pharmaceuticals seem fair, with very modest remaining upside potential over the next two years. However, we are seeing several new compounds coming to markets in the next few years. We try not to get too excited about drug pipelines, but investments in research and development (R&D) have recently started to deliver returns that are more attractive than at any point in the past decade. If this improvement in R&D productivity continues, we can expect more than simply dividend income from these stocks.

Of the most cyclical areas, where are you willing to buy now?

CM: Energy and materials had a terrible 2014, and were two of the worst sectors in every region globally. For materials stocks, the key is to add the lowest marginal cost producers with the strongest balance sheets, and buy incrementally as these stocks continue to underperform global equity markets. We will likely see an improvement in commodity performance at about the same time as consensus argues for an indefinite slump in the commodities cycle. Metals, oil, and every other commodity simply respond to the forces of supply and demand.

Kevin, what supply and demand forces are at play in the energy sector?

KD: From a supply perspective, the addition of Libyan barrels put significant downward pressure on oil prices in 2014. Elevated levels of North American and Iraqi oil outputs are contributing further to the glut. As for demand, weak economic activity in Organization for Economic Co-operation and Development (OECD) member countries since April 2014 accelerated the shrinkage in absolute oil demand in regions including Japan and Western Europe. As the current oil price indicates, non-OECD countries did not accelerate growth enough to pick up the slack. Forecasters generally overestimated demand growth in 2014, and we may see further downward revisions this year. Financial market factors also influence the oil price and can drive it to a level disconnected from the fundamentals in the short term. We witnessed a dramatic liquidation of oil futures beginning in mid-2014 from non-commercial participants—predominately speculators. Traders built long positions in oil futures as geopolitical conflicts with ISIS and Russia threatened supply, and then hastened to close the positions in light of diminishing demand expectations and general commodity price declines. These financial market forces are no small influence—the futures market is about 18x the size of the physical market. We recognize that a meaningful supply upset could happen at any time, given ongoing geopolitical unrest in Libya, Syria, Yemen, Sudan, and similar regions.

Both US and non-US markets have some of the world’s best energy companies, and a well-positioned portfolio should have the ability to choose from the most inclusive investable universe.

Ellen, given that supply growth is outpacing demand, are Brent prices below USD$60 a barrel justified?

EL: Based on fundamentals, the energy market is out of equilibrium. Today’s prices suggest an abundant supply relative to history, and this simply is not the case. Oil inventories remain within a normal range, and spare capacity in the market is extremely low and generally confined to Saudi Arabia. Given Saudi Arabia’s fiscal spending needs, growing domestic demand for oil, and declining per-rig production amounts, it is not easy for them to export at current levels. Their priorities might shift, and the Saudis may reduce oil production by the summer of 2015. Saudi Arabia is allowing the price to fall, but has minimal spare capacity, and is not investing in additional capacity. Oil prices below $60 per barrel pressure the profitability of all producers, regardless of geography, and therefore are unsustainable over any period longer than roughly a year. We also expect the current depressed levels of oil prices to spur consumption, and pull up demand.

KD: Consistent with our approach to the materials sector, we seek the most financially sound energy companies that have substantial cost advantages over competitors. We believe these companies can withstand a period of lower oil prices and benefit from a subsequent rise. Both US and non-US markets have some of the world’s best energy companies, and a well-positioned portfolio should have the ability to choose from the most inclusive investable universe.

*Credit Suisse Securities Research & Analytics, “2015 Outlook: Themes, Sectors and Styles,” Global Equity Strategy, December 18, 2014

Important Disclosures

The MSCI USA Index is a free float-adjusted market capitalization weighted index, designed to measure large- and mid-cap US equity market performance. The MSCI USA Index is a member of the MSCI Global Equity Indices and represents the US equity portion of the global benchmark MSCI ACWI Index. The MSCI EAFE Index is a free float-adjusted market capitalization weighted index, designed to measure developed market equity performance excluding the U.S. and Canada, consisting of 21 stock markets in Europe, Australasia, and the Far East. The Indices are gross of withholding taxes, assume reinvestment of dividends and capital gains, and assume no management, custody, transaction or other expenses. It is not possible to invest directly in these indices. MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

Market Commentary

The market commentary expresses the portfolio managers’ views as of 12/31/2014 and should not be relied on as research or investment advice regarding any stock.

These views and portfolio holdings and characteristics are subject to change. There is no guarantee that any forecasts made will come to pass. Any portfolio securities identified and described do not represent all of the securities purchased, sold, or recommended for client accounts. The reader should not assume that an investment

in the securities identified was or will be profitable.