Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

Passive strategies have garnered an increasing share of institutional mandates within international equities. The starting suppositions of any indexation strategy are, a) you are aware of the risk factors you are taking when establishing this exposure b) the index correctly captures the opportunity set of the asset class in which you are investing, and c) your timing of indexation is correct. Unfortunately, these suppositions are generally incorrect. Read our December newsletter to learn why we believe the merits of investing actively persist in today’s environment.

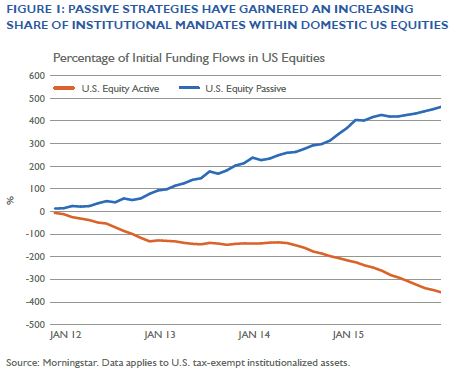

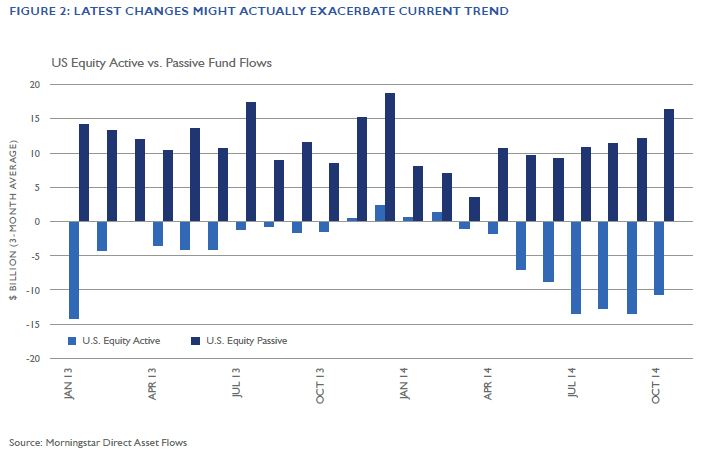

Judging by the flows into passive strategies in recent years, some investors are abandoning active portfolio management with increasing intensity. Morningstar’s round up of 2014 mutual fund flows found that active funds across all asset classes experienced $44 billion of net contributions while passive funds received inflows of $420 billion. Similarly, in the first half of 2015, data from Investment Metrics suggest that passive investing garnered 27% of initial international equity funding by U.S. tax-exempt institutions, up from 3% ten years ago (see Figure 1). Moreover, the Department of Labor’s proposed fiduciary rule could be the catalyst for another sustained wave of passive equity investing. The new standards for financial advisors serving retirement accounts could send $1 trillion in new assets to passive investment products, according to Morningstar (see Figure 2). The starting suppositions of any indexation strategy are, a) you are aware of the risk factors you are taking when establishing this exposure b) the index correctly captures the opportunity set of the asset class in which you are investing, and c) your timing of indexation is correct. Unfortunately, these suppositions are generally incorrect.

Passive strategies have garnered an increasing share of institutional mandates within international equities.

The typical academic argument for passive management goes something like this: It is a well-known truism that investing is a zero-sum game, in which the returns of all active participants, before fees, sum to the return of the market itself. Thus, an index tracking that market will deliver mean performance with some active managers beating it and others losing to it. The argument continues by introducing fees and demonstrating that the average active manager cannot consistently outperform the index, and active management is a fool’s errand dependent on luck and not skill. Finally, since the market is efficient, you’re better off simply investing in a low-cost passive alternative.

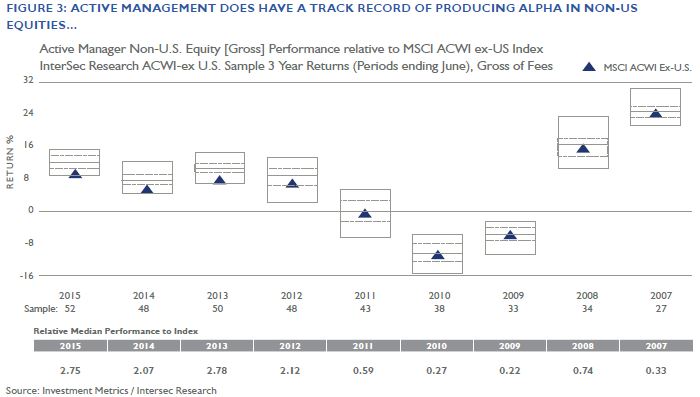

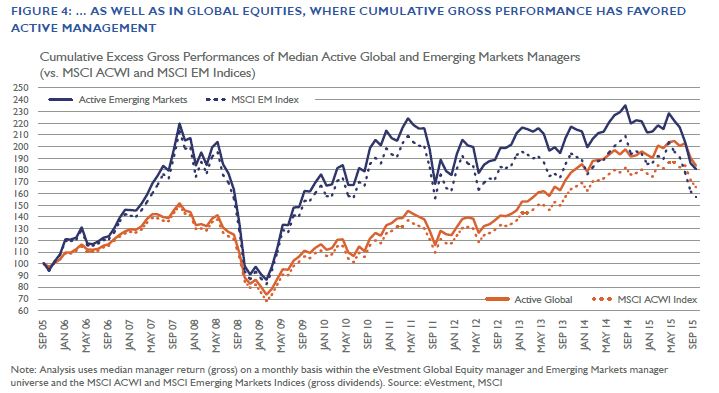

Active management does have a proven track record of producing alpha in non-U.S. equities… As well as in Global Equities, where cumulative performance favors active management.

These arguments, however, ignore three critical facts. First, after fees, index funds have underperformed the index virtually 100% of the time. Second, most of the famous academic studies focus on the U.S. market. Recent data suggest that, for international (and global) equity funds, active managers consistently have beaten the index (see Figures 3 and 4). Third, and most importantly, markets are not efficient and therefore, an index will reflect a myriad of biases at any point in time. Since the factors that drive the returns for any index are not constant, it’s hardly surprising that disciplined active managers experience periods of underperformance. However, even when the annualized excess return to a benchmark, or “alpha,” delivered by an active manager appears to be modest, compounding excess returns over a period of years can add up to significant gains.

Passive investing may have a role in a broad portfolio. However, excluding active management is akin to suggesting that a team that goes 50-50 during a season can never improve on its record and it’s futile to even try. As numerous studies in behavioral science have shown, investors are far from rational. Market participants are prone to deep-rooted psychological predispositions that often cause asset price anomalies. Since these asset price anomalies are always present, the market and representative indices will always reflect a host of inefficiencies. Chief among these are a short-term focus, indifference toward valuation, and disregard for risk.

Since current prices are driven by marginal buyers and sellers, an index’s composition is defined by those short-term influences. Capitalization-weighted indices, which dominate the performance measurement industry, therefore become vulnerable to extreme allocations at certain points in time. In March 2000, for instance, the technology sector represented 65% of the weight in the NASDAQ Composite Index and 33% of the S&P 500 Index. We all know how technology stocks fared over the next couple of years. A decision to index the MSCI EAFE Index in December 1989 when Japanese stocks were at their most expensive (and comprised 60% of the weight in the EAFE Index) would have led to years of poor performance relative to other markets. And finally, financial stocks as a proportion of the S&P 500 Index nearly doubled from the mid-1990’s to 20% by mid-2007. By the end of 2008, they had shrunk to about 11%. Active managers, by contrast, can resist and even exploit these extreme index allocations.

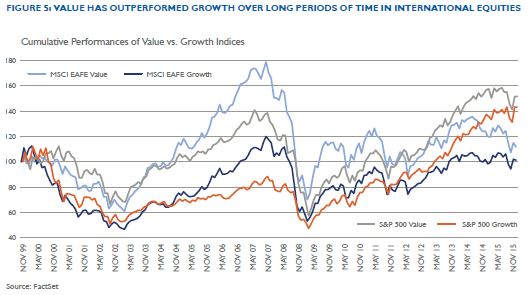

By extension, most indices are indifferent to valuation. Capitalization-based weighting ensures that the largest, most overvalued stocks receive the largest weights. Since an index is dismissive of valuation, it is reasonable to ask what role, if any, valuation plays in the investment decision. All active managers employ some valuation methodologies in their decision making process and, as such, any decision to apply a passive approach to investing is the antithesis of active investing. Note that value style investing over full market cycles has outperformed conventional market capitalization indices. By default, investors in passive funds endorse the current valuation of all stocks in the index. Active managers can build portfolios that take contrarian points of view with regard to valuation.

Ignoring valuation is certainly one of the bigger risks embedded in passive investing. But valuation isn’t the only systemic risk to consider. As we have demonstrated in our recent whitepaper on Causeway’s Risk Lens, country, currency, sector, and style factor risks must all be considered to avoid the potential for excessive factor concentration or unintended factor dependence that may subsequently lead to underperformance. Style investing is cyclical in nature and, coupled with the zero-sum law of investing, can often lead investors to gain exposure to the wrong type of factors at a point in time. The greater an index’s imbalance to one or several of these risk factors, the more concentrated the impact of changes in prices and therefore, the greater the potential volatility. Investors need to know the overall portfolio exposure to such factors. Focusing exclusively on the risk of underperformance versus a benchmark will, in all likelihood, expose the portfolio to a myriad of other risks and unintended consequences. Active managers can control their exposure to specific factors. Causeway, for instance, uses a proprietary risk model which aggregates stock-level factor exposures to the portfolio level. Prospective holdings are rewarded if they diversify the existing portfolio with regard to factor concentrations, and ultimately, our portfolio consists of those stocks with higher expected return relative to each stock’s marginal contribution to risk (or “MCTR”). This enables us to take an objective approach to risk, with no direct reference to the risk factors currently embedded in market indices.

Focusing exclusively on the risk of underperformance versus a benchmark will, in all likelihood, expose the portfolio to a myriad of other risks and unintended consequences.

The timing of a decision to abandon active management in favor of a passive strategy faces a number of hurdles. Often investors decide to index after a manager has underperformed. This may be precisely the wrong time if the factors that have driven short-term performance of the index are unsustainable (e.g. overvaluation or excessive country or sector concentration). If an investor decides to invest passively, the choice of which index to mimic becomes critically important and any decision to change managers, or even to change the allocation, should be based on the same criteria and judgement used to select them.

In assessing the relative merits of active versus passive management, it’s essential to remember that good active managers earn their fees by resisting the inherent biases of markets and indices. These contrarian decisions will inherently involve periodic underperformance versus market indices. In the long run, however, these contrarian decisions can pay off, particularly in international, emerging, and global equity markets where active managers have a consistently positive record of outperforming the relevant index before fees. Causeway prides itself on always retaining a long-term, value-focused, risk-conscious approach as stewards of our clients’ capital.

The newsletter expresses the authors’ views as of 11/30/2015 and should not be relied on as research or investment advice regarding any stock. These views and portfolio holdings and characteristics are subject to change. There is no guarantee that any forecasts made will come to pass.