Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

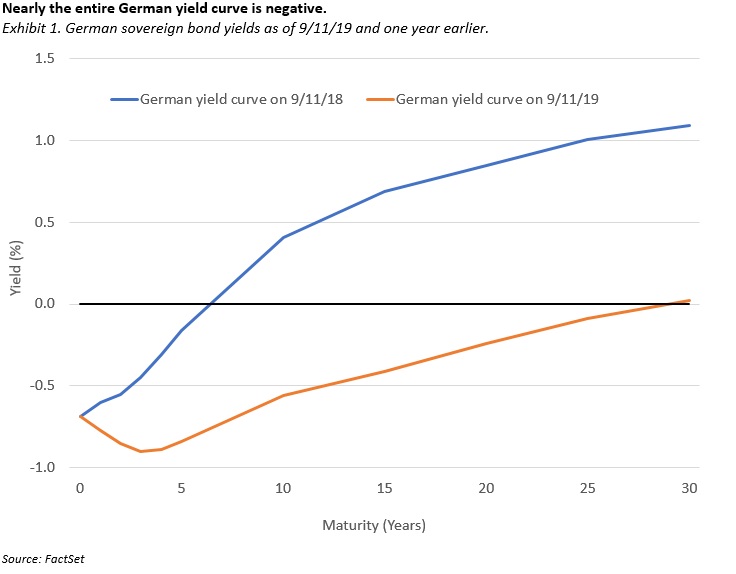

Negative interest rates upend familiar financial relationships, yet they have become pervasive across several developed global markets. Danish banks are paying homebuyers to take out mortgages. Nearly the entire German yield curve was below 0% in early September. Even in the US, the term premium, which represents the additional compensation that investors require to hold longer-term debt, turned negative this year. As of the end of August 2019, the buyer of a 10-Year Treasury bond pays a premium to hold that bond relative to the alternative of rolling over a 1-Year Treasury Bill for ten years.

Key insights

- Supply and demand imbalances are contributing to the growing stock of negative yielding debt.

- An abatement of geopolitical risks and/or increased fiscal government spending could push rates higher.

- We seek companies with higher barriers to entry and operational restructuring. A well-covered dividend yield is especially attractive in this negative yield environment.

What could compel institutional savers to accept losing money on their bank deposits, and bondholders to pay to loan money? How can an equity investor benefit from the likely consequences of this sustained ultra-loose monetary policy?

We begin by examining the magnitude of negative yielding debt.

For highlights of our primer, check out our Causeway Quick Takes video.

How much negative yielding debt exists currently?

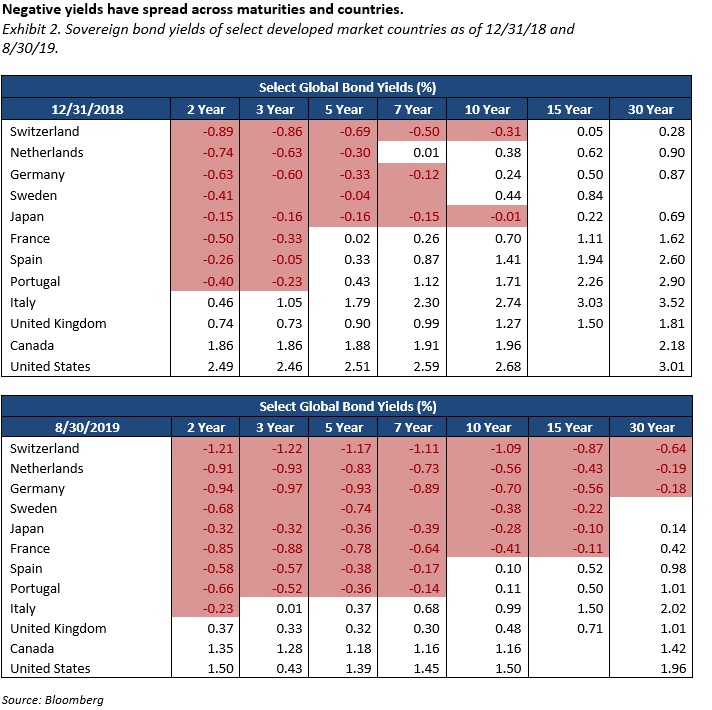

Since December 2018, the amount of debt carrying negative interest rates has increased significantly. Most of this debt is issued in Europe and Japan.

The stock of negative yielding debt has more than doubled, from approximately $8 trillion at the end of 2018 to approximately $17 trillion at the end of August 2019. That means that investors are paying, rather than receiving, interest to hold over a quarter of the global debt market. Negative yielding debt is not limited only to sovereigns—it increasingly includes corporate and mortgage debt as well.

Why are interest rates currently negative?

The sudden drop in the term premium in 2019 and the increase in the stock of negative yielding debt is, we believe, due to a supply and demand imbalance. The demand for safe haven assets, particularly from institutional investors like pension funds, with few other options for low-risk assets, has outstripped supply. European financial institutions must own these bonds, even if negative yielding, to satisfy central bank-imposed liquidity regulations. Some investors have directed capital flows to safe haven assets in response to rising geopolitical risk and expectations for a slowdown in the global economy. Demand for negative interest rate bonds likely also reflects investor expectations of additional sizable monetary stimulus from the European Central Bank (“ECB”) and Bank of Japan (“BOJ”). With this support in place, investors expect to sell the bond at an even higher price/lower yield. Excess savings in the aging developed economies has likely arisen for several reasons, including demographics, the shift to less capital-intensive, more service-oriented economies, and the significantly reduced level of investment following two decades of massive Chinese industrialization.

By massively expanding their balance sheets, central banks have effectively removed large amounts of sovereign, mortgage and corporate bond supply from the market.

Not only has demand risen, but also a supply shortage has occurred globally. By massively expanding their balance sheets, central banks have effectively removed large amounts of sovereign, mortgage and corporate bond supply from the market. For example, the BOJ is buying the lion’s share of Japanese government bonds (“JGBs”), and it also owns approximately 77% of Japan’s overall exchange-traded fund market. That does not leave much for anyone else, exacerbating the supply shortage of JGBs.

What might spur a rise in rates?

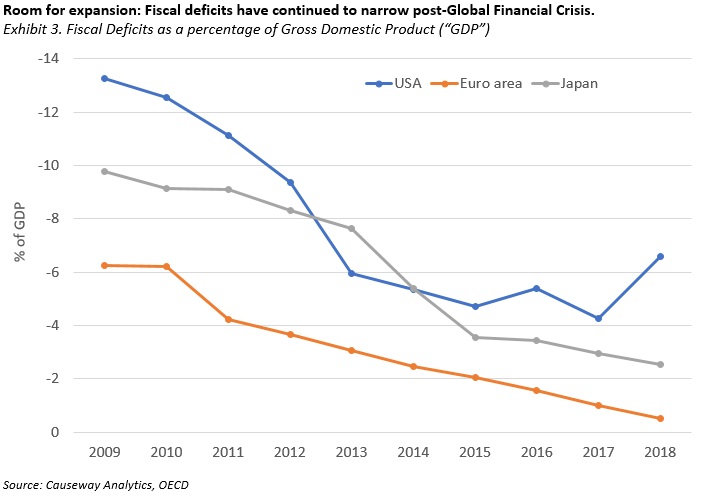

A resolution to geopolitical risks, including the US-China trade war, Brexit, and Hong Kong protests, could propel the term premium into positive territory. Furthermore, any significant and sustained rise in inflation expectations would likely push up interest rates. With low/no cost of financing, governments may decide to use fiscal policy more aggressively, especially if they believe that monetary policy options are exhausted. In a negative rate environment in which some governments are paid to borrow, costless funds can fuel fiscal expansion. According to Modern Monetary Theory, a sovereign can expand its central bank balance sheet and engage in fiscal stimulus until inflation becomes a problem. Central banks remit any interest earned to their country’s treasury, and perpetually roll over principal, obviating the need to repay debt.

We believe that policymakers have every incentive to use fiscal stimulus as a policy tool to reinvigorate economic growth. The rise of populism may amplify this spending trend. From tax cuts, to infrastructure spending, to addressing climate change, fiscal stimulus may lead to an upturn in investment spending. This type of stimulus in the G7 countries and in China should also benefit a wide array of emerging countries, bolstering their domestic growth.

What are the implications for equity investors?

As interest rates nosedived over the year-to-date period, equity investors intensified their “overreach” for yield, crowding into economically defensive stocks (perceived as bond proxies), regardless of their valuation multiples. Through the end of August, momentum attracted more buying, and cyclicality attracted more selling. We believe that prices of many cyclical stocks, as well as other undervalued segments of global equity markets, already reflect slowing economic growth, heightened trade tensions, a disorderly Brexit, and possibly other headwinds to growth.

At Causeway, we incorporate the following considerations into our bottom-up, value-oriented research process:

Identify companies with barriers to entry

For each industry, we recognize that competitors and potential new entrants have access to low cost debt capital. As a result, the importance to us of identifying businesses that have non-capital based barriers to entry increases. At Causeway, we are redoubling our efforts to identify mispriced companies that both generate and sustain cash flows in a low interest rate environment.

Emphasize operational restructuring

Causeway seeks to invest in companies where the management teams are implementing operational restructuring (self-help) that will boost earnings regardless of the economic climate ahead. While we wait for an upturn on earnings and share price, we expect these companies to return capital to shareholders.

Consider second order benefits

Investors have seemingly abandoned certain market segments that are vulnerable to a low/negative interest rate environment. But positive second order effects can partially offset these challenges. For financial services stocks, a mainstay of value-oriented portfolios, we believe the market already has more than priced in the revenue headwinds associated with a prolonged period of low/negative interest rates. But, a sustained period of extremely low rates also leads to below-normal credit losses, which is a positive for earnings, by facilitating easily manageable debt service ratios for businesses and consumers.

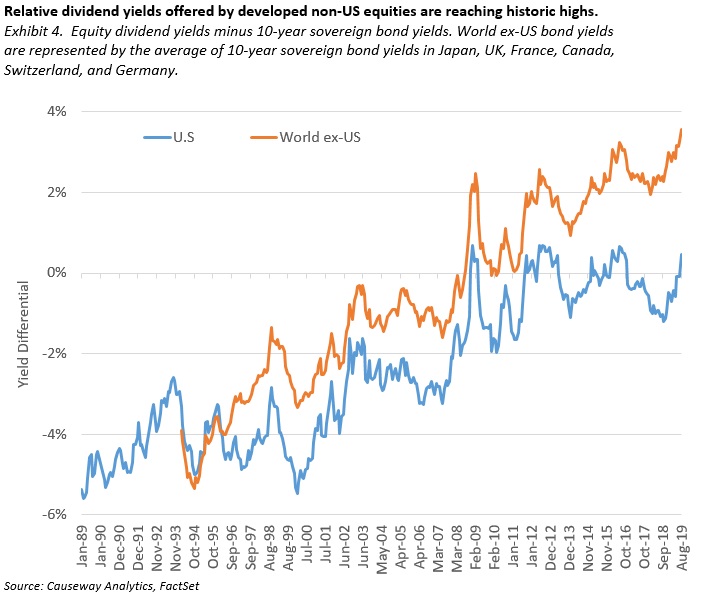

Compared to sovereign bond yields, the dividend yields offered by developed non-US equities are particularly attractive relative to history.

Benefit from share buybacks and attractive dividend yields

In the current environment, share buybacks funded by cheap debt often makes sense. Furthermore, sustained generous dividend payouts from portfolio companies creates an enviable income stream in this low interest rate world. Compared to sovereign bond yields, the dividend yields offered by developed non-US equities are particularly attractive relative to history.

Based on our experience in past market cycles, it is essential to own the out-of-favor investment style before the turn occurs in order to participate in the full recovery.

Be well positioned for the turning point

We believe that value stocks should outperform when markets begin anticipating economic recovery. Furthermore, any sign of rising government spending will likely bolster GDP growth and favor value stocks. If interest rates bottom and start to rise, this should also favor deeply discounted share prices over the expensive segments of markets, especially where high share prices coincide with long duration cash flows. The first two weeks in September illustrated this relationship as the US 10-Year Treasury Yield increased and value stocks outperformed over this period. Based on our experience in past market cycles, it is essential to own the out-of-favor investment style before the turn occurs in order to participate in the full recovery.

Growth in negative yielding debt has confounded financial markets and created valuation distortions across asset classes. In global equities, the scramble for safe-haven assets has put substantial selling pressure on economically cyclical stocks, creating what we believe is a fundamentally unjustifiable valuation discount. For our fundamental portfolios, we use diligent, bottom-up research to uncover the most attractive of the unpopular stocks, which we believe are poised to rebound.

This market commentary expresses Causeway’s views as of September 2019 and should not be relied on as research or investment advice regarding any stock. These views and any portfolio holdings and characteristics are subject to change. There is no guarantee that any forecasts made will come to pass. Forecasts are subject to numerous assumptions, risks and uncertainties, which change over time, and Causeway undertakes no duty to update any such forecasts. Information and data presented has been developed internally and/or obtained from sources believed to be reliable; however, Causeway does not guarantee the accuracy, adequacy or completeness of such information.

International investing may involve risk of capital loss from unfavorable fluctuations in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations.