Contact Us

Subscribe to Causeway Insights, delivered to your inbox.

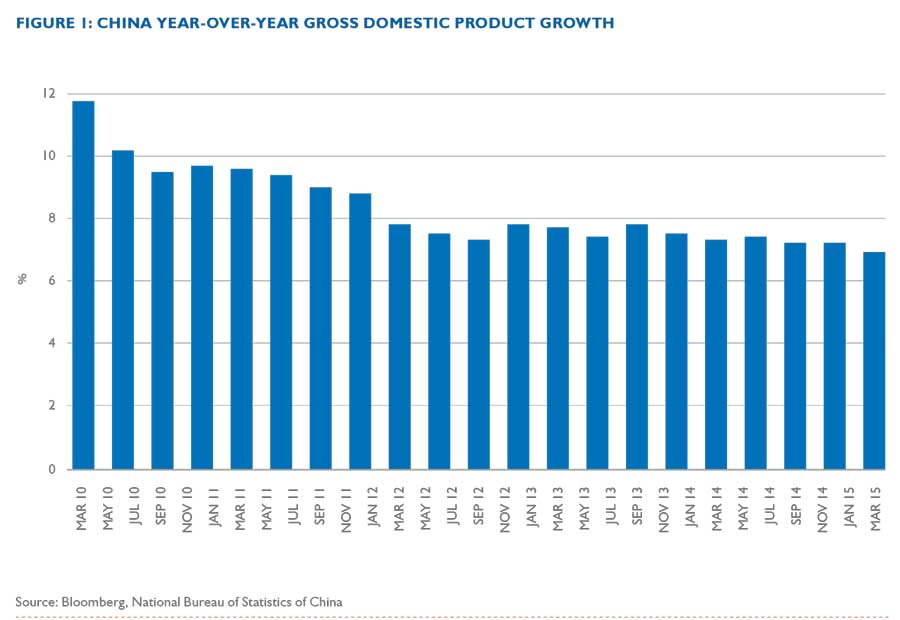

How has the deceleration in Chinese real gross domestic product growth and the government’s boosting of stock markets shaped how we have positioned client portfolios? Causeway portfolio managers present our fundamental and quantitative research view of China in 2015.

Quoted by China Daily newspaper on June 10, 2015, Goldman Sachs Chairman and CEO Lloyd Blankfein commented that “China has achieved a very high growth rate at some cost…so growth has to be absorbed, mistakes have to be corrected and bad investments have to be written off in order to have another stage of rapid growth.” Easier said than done. What are the implications for a slowing Chinese economy—one that cannot absorb the world’s non-food commodities at the pace of the past two decades? China needs to continue its implementation of structural reform (opening industries to foreign competition and lowering trade barriers, for example). This year, the Chinese government’s attempts to rein in margin debt of mainland buyers of domestic A-shares contributed to an aggressive sell off in mid-June. The government announced drastic measures to stem the bleeding in local markets, such as suspending trading and halting IPOs, strongly encouraging companies to engage in share buybacks, and providing unlimited financing to the state agency that supplies capital to Chinese brokers. We consider this intervention to be a step backward. China has set a goal for a more transparent and efficiently functioning financial system, and will likely pay a steep price for misguided policy.

China has set a goal for a more transparent and efficiently functioning financial system, and will likely pay a steep price for misguided policy.

How has the deceleration in Chinese real gross domestic product growth and the government’s boosting of stock markets shaped how we have positioned client portfolios? We spoke to Causeway portfolio managers, Arjun Jayaraman and Jonathan Eng, to understand our quantitative and fundamental research view of China in 2015.

Arjun, how do Causeway’s emerging markets portfolios reflect the team’s expectations for China?

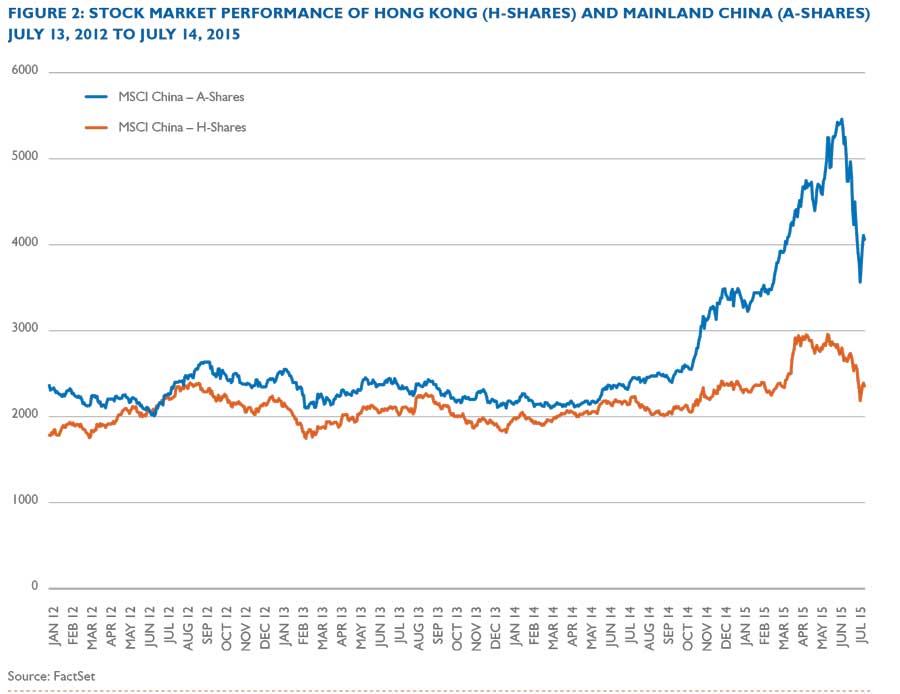

AJ: In order to put some level of support under the local stock market and sustain economic activity, China will probably maintain an accommodative monetary policy. Today, in our unconstrained portfolios, our overall exposure to China is roughly in-line with that of the MSCI Emerging Markets Index (“EM Index”). However, for the past two years we have maintained an underweight position in Chinese banks, a mirror image of the country’s economic health. We recognize the importance of Chinese Hong Kong-listed “H-shares” in the EM Index, but want to lower our emerging markets portfolios’ China risk. In addition, recently we decreased our sensitivity to the Chinese market by adding lower beta (index sensitive) Chinese stocks to our portfolios.

We recognize the importance of Chinese Hong Kong-listed “H-shares” in the EM Index, but want to lower our emerging markets portfolios’ China risk.

Jonathan, Causeway’s international and global value equity portfolios have both direct H-share holdings as well as indirect Chinese exposure by investing in many companies with operations, revenues or other connections to China. As an expert in industrials, how do you view the China exposure in developed markets portfolios?

JE: Speculative booms and busts have—and will –occur in many geographies. Valuations become overextended, share prices fall, investors lose money, then retreat, and valuations return to more rational levels.

Unfortunately, the Chinese government has interfered with the local stock market, one of the most important free market mechanisms. But where does intervention stop? As a research team, we are now contemplating the ramifications of “national” policy to support employment and the extent to which it drags on Chinese corporate earnings. Cutting employees may become very challenging for Chinese companies, especially those that are state-owned. Compared to 2013, we have lowered our global and international portfolios’ weights in capital goods companies. Many of these multinational firms generate a sizable portion of their profits in China. They are vulnerable to deflation, particularly as Chinese demand slows for their products. We have placed more emphasis on spending by the Chinese consumer with holdings in such sectors as consumer discretionary and mobile telecommunications. For example, China’s vehicle ownership is less than 20% the level in the United States; car penetration will likely rise with improved affordability. Furthermore, the government has accelerated the replacement cycle and wants to remove the old, dirtier vehicles from the road. We are also looking at a sanguine outcome for luxury goods demand and tourism.

With surplus capacity in basic industries, China needs a solution to absorb its years of excess fixed investment. What are you anticipating?

JE: I think the government has already signaled its intent to export some of its construction and industrial excess capacity, as well as newer technologies in solar panel, machinery and telecommunications equipment, via the Silk Road Economic Belt and Maritime Silk Road (aka the Belt and Road initiative). This development strategy, first announced in late 2013, is designed to boost employment in China, as well as accelerate more capital convergence and currency integration globally, lessening dependence on the US dollar.

AJ: By investing in transportation and other commercial infrastructure (highways, railways, ports, and coastal facilities) across Asia, the Middle East, and Europe, China intends to improve trade and foreign relations, and find a productive home for its massive $4 trillion of foreign reserves. In our emerging markets portfolios, we increased exposure to Chinese-listed industrials companies that we expect to benefit from the Belt and Road initiative. However, by interfering with its own stock market, China has apparently postponed its drive toward a more market-based mechanism of resource allocation.

We have placed more emphasis on spending by the Chinese consumer with holdings in such sectors as consumer discretionary and mobile telecommunications.

Beyond the stock market, speculation also appears rampant in residential housing. What are the economic and portfolio implications of this housing risk?

JE: Housing remains an important store of value for the Chinese saver. We do not believe that the current overbuilt situation and vacant units are systemically dangerous, but they are additional examples of oversupply.

A sustained fall in house prices nationwide would likely crimp consumer spending, but not the banking system. House buyers either pay in cash or use modest levels of debt. Assuming rural-to-urban migration continues, low-end units in tier 2, 3, and 4 cities should experience rising demand. We have generally sought to avoid positions in Chinese property following the onset of speculative housing fever in 2010-11.

AJ: Ironically, weakness in the Chinese A-share market may help support local housing prices. In addition to housing, the only real investment choices for the retail investor are domestic equities, bank deposits, some wealth management products and (for those with the highest incomes) overseas investments. Volatility in the Shanghai stock market is teaching the highly-levered local investor a tough lesson about valuation. Through this year’s Shanghai-Hong Kong Stock Connect program and the recently implemented mutual fund recognition initiative, the Chinese government continues its efforts to facilitate cross-border investment between foreign institutional investors and the mainland. Assuming market connectivity and capital mobility improve, the enormous premium of A-shares relative to H-shares should eventually erode. The government’s market manipulation stymies this effort to bring best practices to China’s undeveloped markets. Despite this setback, we are still convinced that those best practices will eventually take hold in China, to benefit all investors.

Important Disclosures

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

Market Commentary

The market commentary expresses the portfolio managers’ views as of 7/15/2015 and should not be relied on as research or investment advice regarding any stock. These views and portfolio holdings and characteristics are subject to change. There is no guarantee that any forecasts made will come to pass. Any portfolio securities identified and described do not represent all of the securities purchased, sold, or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.